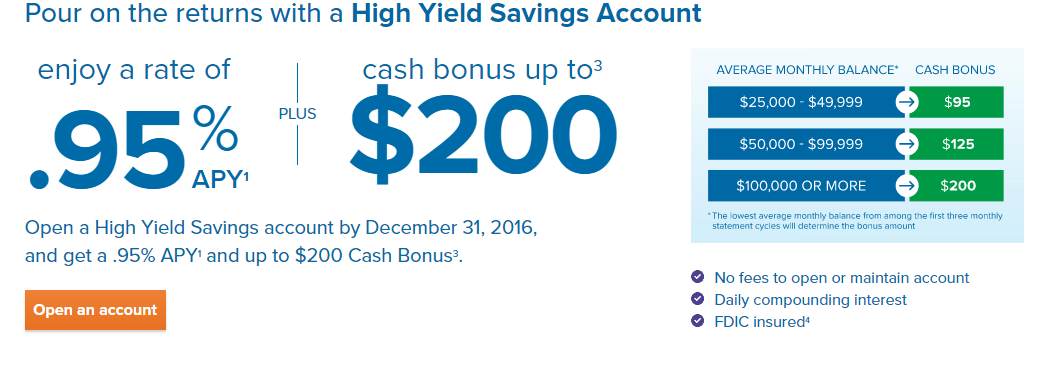

Offer at a glance

- Maximum bonus amount: $200

- Availability: Nationwide

- Deposit Required: $25,000-$100,000

- Deposit Length: 3 statement cycles

- APY: 0.95%

- Hard/soft pull: Soft

- ChexSystems: Unknown

- Credit card funding: Unknown

- Monthly fees: None

- Early account termination fee:

- Expiration date: December 31st, 2016

The Offer

- Open a High Yield Savings Account with CIT Bank (0.95% APY) and receive a bonus of up to $200, the bonus you receive depends on how much you deposit. You’re required to keep that average minimum daily balance for three statement cycles. The tiers are as follows:

- $25,000-$45,999: $95

- $50,000-$99,999: $125

- $100,000+: $200

The Fine Print

-

Limited time Bonus offer valid on High Yield Savings accounts opened and funded on or before December 31, 2016, provided that the following requirements are met:

- The account is opened with a minimum initial deposit of $25,000 not already on with or help at CIT Bank, N.A. or its OneWest Bank division.

- An average monthly balance of at least $25,000 is maintained in the account through the first three full statment cycles. How we calculate the average monthly balance for each statement cycle: at the end of each day, the High Yield Savings account balance is recorded. When the statement cycle ends these end-of-day balances are added together and then divided by the number of days in the statment cycle to determine the average monthly balance.

- If the opening deposit is less than $25,000, if the account is closed prior to the end of the third statement cycle or if the average monthly balance from any of the first three statement cycles is less than $25,000, the account will be deemed ineligible for a bonus payment.

- Any Bonus for which the customer qualifies will be deposited to the account within 30 days of the end of the third monthly statement cycle.

- All bank account bonuses are treated as income/interest and as such you have to pay taxes on them

Avoiding Fees

There are no monthly fees and no early account termination fee.

Our Verdict

The upside to this savings sign up bonus is that it offers a reasonable APY of 0.95%, the best current rate for non rewards accounts is 1.25% so you’re losing out on 0.3% APY but obviously get this bonus. If you put $100,000 for three statement cycles you’d be losing ~$75 in interest, so the top tier bonus is really only $125. For the other bonuses you’d be earning more (total bonus of $380 if you put $25,000 into 4 accounts across 4 people) but you’re also having to open four accounts instead of just one (and you could have opened another banka ccount bonus instead).

I doubt many readers will have these types of funds available in cash, but if you do it’s probably worth putting it into one of the rewards checking accounts instead (one with a higher maximum balance preferably).

This assumes that it’s a soft pull to open the account and there is no credit card funding. If it’s a hard pull it’s even worse of a deal as you could get a nice credit card cash sign up bonus instead. If you can fund a huge amount with a credit card then it might be worth opening just for that. Please share your experiences in the comments.

Useful posts regarding bank bonuses:

- A Beginners Guide To Bank Account Bonuses

- PSA: Don’t Call The Bank

- Introduction To ChexSystems

- Banks & Credit Unions That Are ChexSystems Inquiry Sensitive

- What Banks & Credit Unions Do/Don’t Pull ChexSystems?

- How To Use Our Direct Deposit Page For Bank Bonuses Page

- Common Bank Bonus Misconceptions + Why You Should Give Them A Go

- How Many Bank Accounts Can I Safely Open Within A Year For Bank Bonus Purposes?

- Affiliate Links & Bank Bonuses – We Won’t Be Using Them

- Complete List Of Ways To Close Bank Accounts At Each Bank