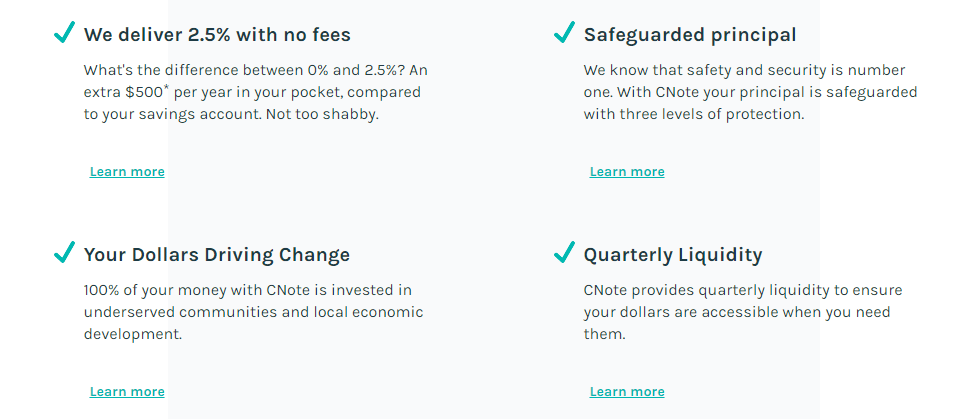

CNote is a ‘alternative’ savings account that invests your money in small businesses and communities in America and advertises 2.5% APY. Unlike other savings accounts this is not insured at all, normally a savings account is either FDIC insured or NCUA insured.

CNote lends money exclusively to Certified Community Development Institutions (CDFIs), they discuss this in more detail here. They show that the net charge off rates are lower than FDIC insured products, keep in mind that when a FDIC insured institution fails your accounts are still covered up to $250,000. Whereas when a CDFI fails you the investor are on the hook if their ‘triple protection plan‘ fails. Part of that plan includes a loss reserve fund that CNote mantains, but no details are listed on the amount in this fund and the total amount lended through Cnote so it’s difficult to get any peace of mind from the this. Unlike a traditional account CNote’s account you cannot access your funds whenever you want. You’re instead given quarterly liquidity with a 30 day notice.

Our Verdict

Personally I don’t recommend putting funds into an uninsured account like this, especially when you’re able to get a 2% APY rate with an insured account (or up to 5% on an insured rewards account). I guess some people will be tempted due to the community angle but you’re not given any say on which projects are/aren’t funded and given that these are low risk projects anyway I suspect most of them would be funded without CNote. I guess this is kind of a bit like Kiva but for American small businesses and community projects and you get a return but you don’t get to pick your projects.