Update 11/10/20: See better offer here.

Update 11/1/20: More people are being targeted for the 75,000 offer via snail mail.

The Offer

American Express Gold Card link

Until today, the standard/high signup bonus on the American Express Gold card has been 50,000 points with $4,000 spend. A few new offers came out today:

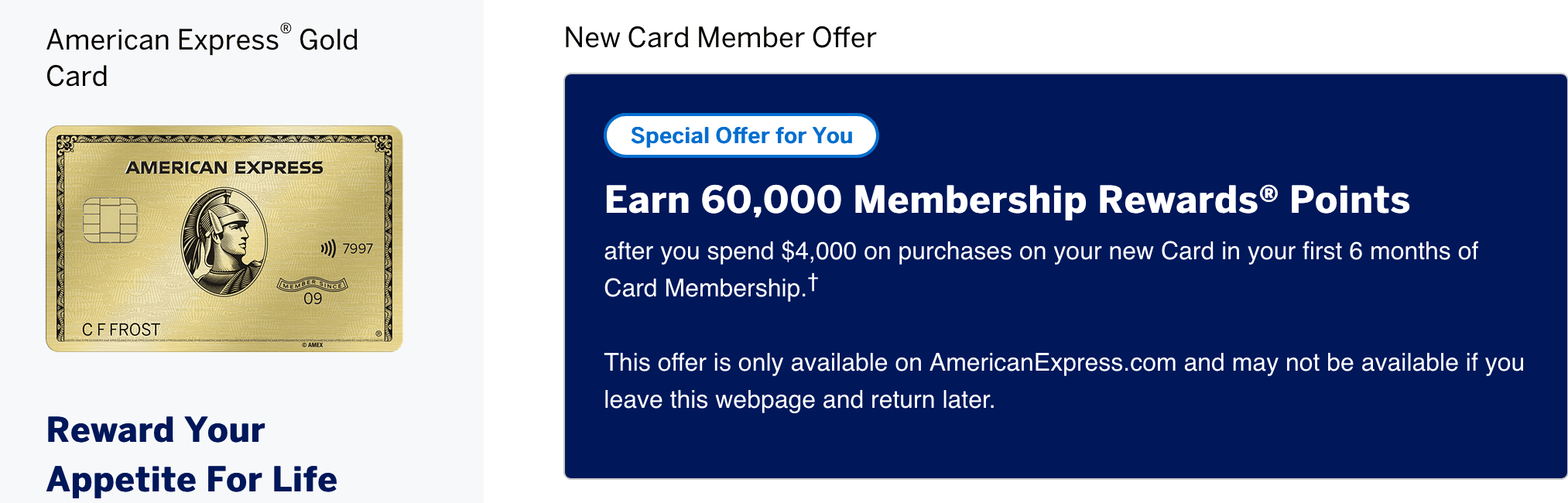

- New public offer: Get 60,000 points signup bonus when spending $4,000 within 6 months.

- This offer is showing for some both on the public signup page and via referral link. If you don’t see it, try a few browsers, incognito, etc, to get it to show. I got this one in Firefox.

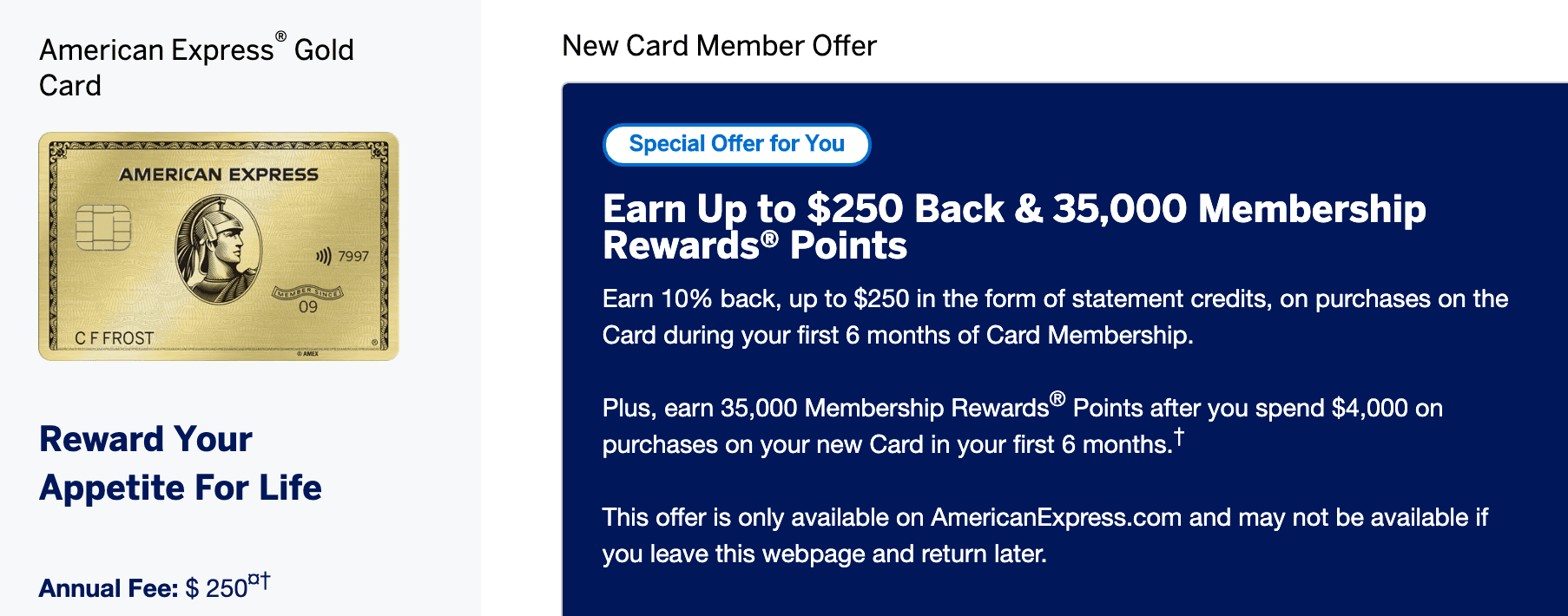

- Alternative new public offer: Get 35,000 points signup bonus when spending $4,000 within 6 months. Plus, get 10% back as a statement credit on purchases made during the first 6 months of Card Membership, up to $250 back.

- This offer is showing for some both on the public signup page and via referral link. If you don’t see it, try a few browsers, incognito, etc, to get it to show. I got this one in Chrome incognito.

- We already posted about the new public Resy offer: Get 35,000 points signup bonus when spending $4,000 within 3 months. Plus, get 20% back as a statement credit when you make a purchase at restaurants worldwide within the first 12 months of Card Membership, up to $250 back.

- New targeted pre-qualified offer: Get 75,000 points signup bonus when spending $4,000 within 6 months.

Card Details

- Annual fee of $250 NOT waived first year

- Card will earn at the following rates:

- 4x points at Restaurants

- 4x points at U.S. supermarkets (up to $25,000 in spend per calendar year)

- 3x points for flights booked directly with airlines

- 1x points on all other purchases

- $120 dining credit. This is a $10 monthly credit that can be used at Grubhub, Seamless, The Cheesecake Factory, Ruth’s Chris Steak House, Shake Shack

- $100 airline fee credit

- No foreign transaction fees

- Full American Express Gold card review can be found here.

Our Verdict

Standard high bonus on this card has been 50,000 points after $4,000 in spend. We have seen 50,000 + $100 in the past, as well as a targeted 70,000 offer too.

These new offers are pretty interesting:

- Obviously the 75,000 offer is terrific and highest ever. It even gives 6 months to meet the spend. Only works for someone targeted with the pre-qualified tool.

- The 60,000 public offer is quite good, and most will consider it superior to the other two statement credit offers (you’re essentially buying 25,000 MR points for $250). It’s especially a powerful offer when you combine with a referral link since your friend will then get up to

25,00030,000 points for the referral as well. From this angle, the 60k offer can potentially be better than the 75k targeted offer. - Cashback aficionados might prefer the 10% statement credit offer. That’s for someone who values Membership Rewards points at 1 cent or less.

- The Resy offer isn’t really useful for anyone.

If you’re thinking of applying, make sure you read these things everybody should know about American Express cards first.

Thanks to those who tipped us off to this deal.