Background

Those of us who are into Manufacturing Spend have certainly heard about the deluge of shutdowns on the Amex Old Blue card. It first started on October 22, and we plodded along for a month and a half with no major developments on this front, besides more-and-more people reporting shutdowns. There’s been shut downs reported as recent as December 13.

Two discussions on Flyertalk that I did find interesting:

- Whether or not those who were shut down were able to apply for new Amex cards – some were and some weren’t. Some who were denied new cards were able to get approved with a reconsideration call. Another amazing point is that some people applied for a new Old Blue card and got instant approvals!

- Some tips were discussed for those who were shut-down on how they could very likely get the Reward Dollars that they had earned.

More recently, we reported the news that Amex capped the annual rewards.

The Cap

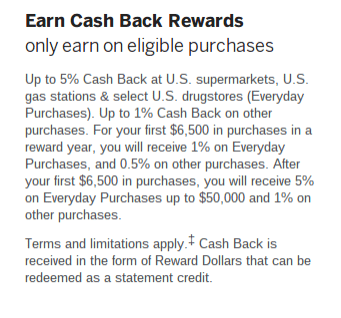

If you look at the Old Blue signup page (which is still live-and-kicking), you’ll see that Amex added a cap on the annual category-spend: $50,000.

This is the same cap that Chase puts on some of their Ink cards. Amex is now adopting that cap for Old Blue.

There’s a lot of talk on Flyertalk if people who already have the card are grandfathered in without a cap, but many of us assume (myself included) that until Amex says something, the new cap does not apply for old accounts, and we can earn 5% on more than $50,000. It’s definitely possible that Amex will soon update the terms for all of us, but until then, it’s hard to hear that the terms have changed.

Of course, this may not be too useful, being that heavy-hitters are getting shut down, and many of us who weren’t shut down aren’t spending such high volume on the card.

Implications

This would seem to imply that 50k is considered okay by Amex, but of course nothing is guaranteed. On Flyertalk, there’s some effort to see if anyone who spent less than $50,000 in category spend got shut down. I don’t believe there’s been a clear report of an under-$50k shut down.

This would mean more a few months down the line, let’s assume the shut-downs stop, that we can possibly use the number 50k as an amount that’s somewhat “safe” to spend. It’s a big scale-down on the usefulness of the card, but it’s still something.

Technical Crunch

For those with the head right now to crunch the numbers, the optimal initial-spend pattern just changed for those with the new capped card. Until now, most of us put the initial $6500 on category spend which would earn 1% as opposed to .5%. Or we split it between category and non-category.

But with the new numbers, it would seem that in order to optimize, you should put the entire initial $6,500 in non-category spend. This way you’re not eating into your $50,000 annual limit with the initial spend. After putting $6,500 non-category, wait for the statement to close, and then put $50,000 of category spend, and you’ll get 5% on the entire $50,000 of category spend. (HT: datch)

Hopefully, this makes sense.

[UPDATE 1/30/15: From the language of the new Old Blue terms it sounds to me that this is incorrect, and you should be able to earn 5% on a full $50,000, even if the initial $6,500 was category spend.]

Fascinating Saga

I personally find the whole Old Blue saga fascinating and perplexing. We see that the Old Blue signup link is not publicly advertised, and this would appear to be a final faze-out of the card.

Yet, the card is still available via the back-link, and Amex is still actively approving applications as we speak. Not only that, they’re updating the terms of the card and making caps on rewards.

If this was a currently advertised card, it would make sense to tweak it and put new limits. But if it’s a card they’re no longer advertising, and it’s being abused, you’d think the first thing they’d do is pull the application link so that no people are added to the gravy train. Then they could start putting caps on existing member, or shutting down existing members.

The only explanation that seems to make sense is the right-hand left-hand theory. There are different departments dealing with available-cards and dealing with rewards. The rewards department sees too much money going into the rewards on this card so they start shutting people down, and they now put a cap on the rewards for new members. But the available-cards department hasn’t decided that they want to completely shut down the card at this time.

Anyway, I find it fascinating. If anyone has any explanatory ideas, I’d love to hear in the comments.

Final Thoughts

The FlyerTalk wiki declares that, “this card is no longer a viable MS instrument“. Personally, I’d still find it nice to be able to get $50,000 out of it. An extra 5% category spend of around $4k per month is still something to consider, despite the initial $6,500 threshold which is necessary to meet.

I haven’t been shut down, but I do consider the card somewhat dead, temporarily, since I’m still a little nervous to spend even at these low levels. Hopefully, the shut downs will stop and we’ll be able to use it in a more limited way without having to worry much.