Thanks to an anonymous source, we’ve finally gotten screenshots of the soon-to-be-released Bank of America premium card. The most important bit of news is that points are worth a flat 1¢ when redeemed as cash.

There are lots of interesting tidbits in these screenshots:

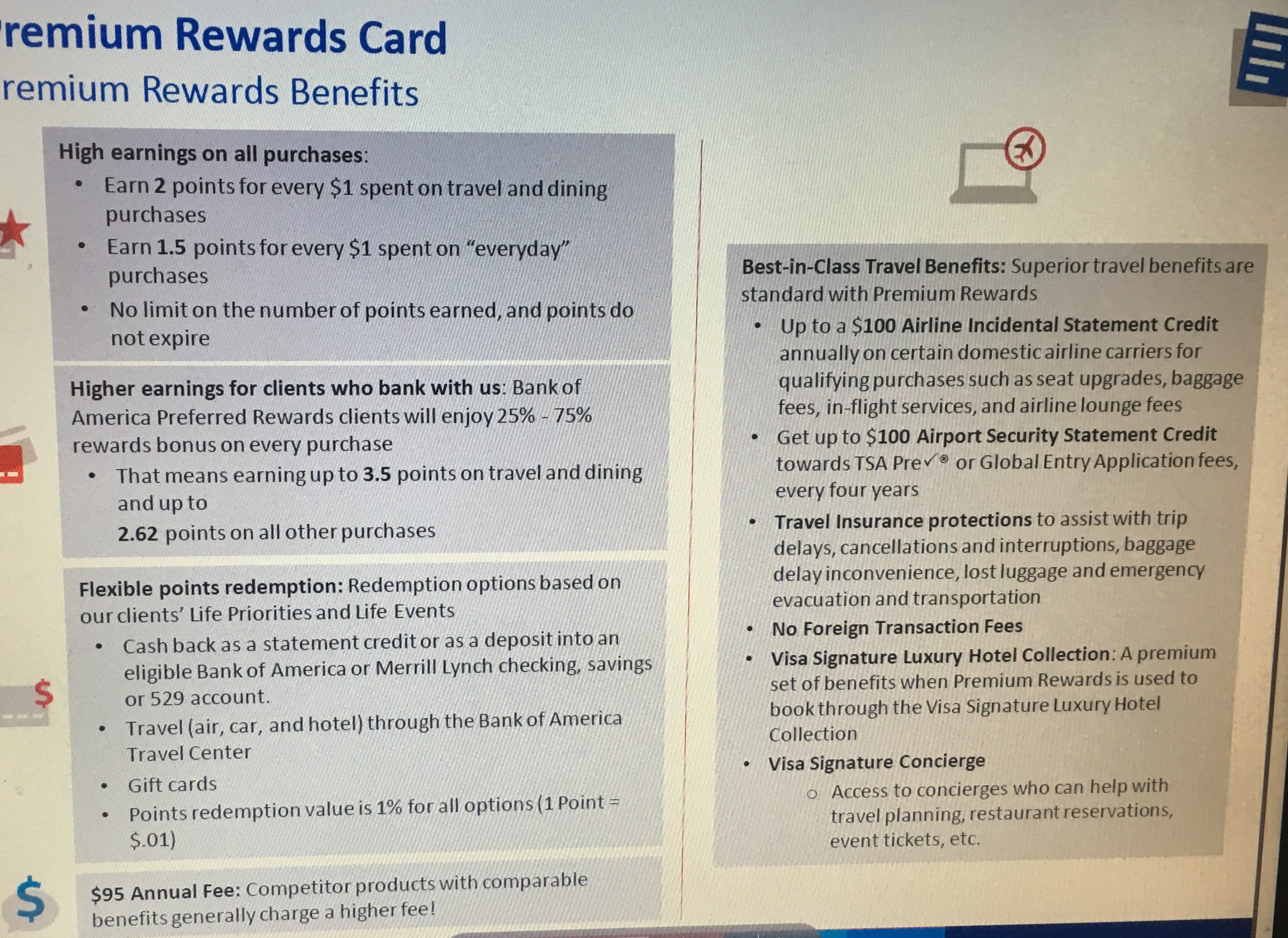

- Biggest news to me is that this card will earn cash back, not travel credits. “Points redemption value is 1% for all options (1 Point = $.01).” Either as a statement credit or a deposit into a BofA account.

For some this barely makes a difference, but for a lot of us it does, and this becomes another reason to choose the premium card over the Travel Rewards card. I wonder if it’ll be possible to transfer Travel Reward points to the premium card and cash them out that way. - $100 Global Entry Fee will be once every 4 years.

- $100 airline incidental credit will only work for domestic airlines, apparently.

- A bit more info here on where the $100 airline incidental credit can be used: seat upgrades, baggage fees, in-flight services, and airline lounge fees.

- Visa Signature Luxury Hotel Collection and Visa Signature Concierge. This isn’t my thing, but I think these are standard Visa Signature benefits?

- Travel insurance protections. We’ll have to wait for the full details to see how it compares.

- These screens seem clear that they are after the affluent, relationship customers with the new card.

- I don’t understand the math in their Chase vs. BofA comparison at the bottom. I think they mean to compare the Sapphire Preferred (not Reserve), but I still don’t get it. $1,000 is earning 2x and $4,000 is earning 1x. That’s 6,000 points which would amount to $75 in travel when booking at the 1.25% rate with Chase Travel, not $77.50.

Target release date on the card is still for mid-September (as per the anonymous source).

Here’s a roundup of all details we know about the card:

- Annual fee will be $95

- No foreign transaction fee

- $100 domestic airline incidentals credit, including seat upgrades, baggage fees, in-flight services, and airline lounge fees mid (does not include airfare)

- 50,000 points signup bonus with $3,000 spend threshold

- 1.5x everywhere and 2x on travel/dining; Preferred Rewards customers will get up to 2.6 everywhere and 3.5 on travel/dining

- It will roll out in mid-September

- It will be a Visa Signature card

- There will also be $100 Global Entry/TSA PreCheck credit once every four years

- Points can be redeemed for cash at $.01 per point