Deal has expired, view more Staples deals by clicking here.

The Offer

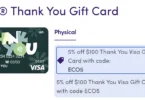

- Staples stores will offer fee-free $200 Visa gift cards for the week of 1/13-1/19. That’s a savings of $6.95.

The Fine Print

- Valid 1/13/2-1/19 (starts Sunday)

- In store only.

- Subject to availability.

- See gift cards for details, terms, conditions, and (if applicable) fees.

- Limit 1 per customer.

- All trademarks are property of their respective owners.

- Product may not be available in all states.

- The gift cards featured are not sponsors of or otherwise affiliated with this company.

- The Visa Gift Card is issued by MetaBank®, Member FDIC, pursuant to a license from Visa U.S.A. Inc.

- Card can be used everywhere Visa debit cards are accepted in the U.S. No cash access.

Our Verdict

Fine print says it’ll only work for a single card per transactions. Although in the past multiples have worked in the same transaction. Make sure to use a card that earns at a high rate at office supply stores, there is also an amex offer and a chase offer. Personally wouldn’t risk using AmEx.