Update: 01.03.18 rate has decreased to a maximum of 1.6% now

Reposting 12/19/17 since rate has increased again, up to 1.75% now.

Reposting 12/14/17 since top rate increased to 1.60% APY from 1.5%. They also offer a ten day guarantee so if the rate increases within 10 days of funding account they will automatically increase the APY after that ten day period.

Offer at a glance

- Interest Rate: Up to 1.6% APY

- Minimum Balance: None

- Maximum Balance: None

- Availability: Nationwide

- Insured: FDIC

The Offer

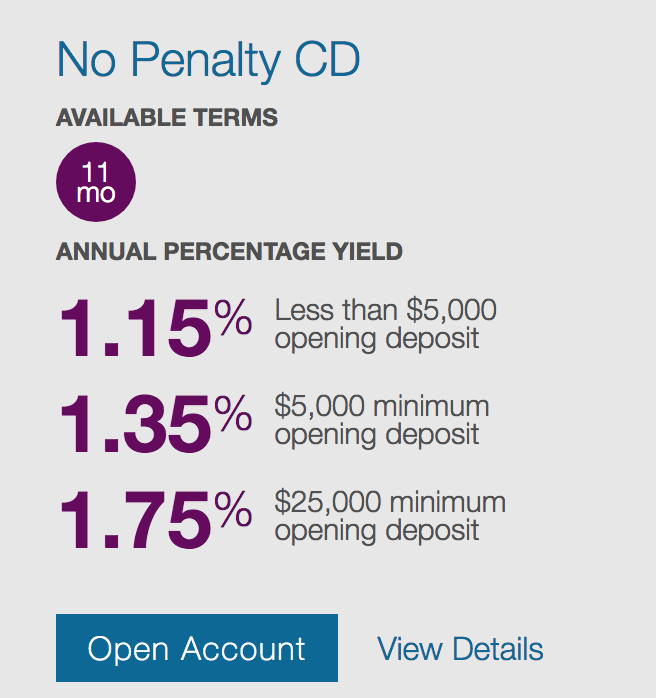

- Ally Bank offers 11 month certificated deposits with the following rates:

- 1.15% for opening deposits less than $5,00

- 1.35% for opening deposits $5,000-$25,000

- 1.75% for opening deposits $25,000+

The Fine Print

- As long as the account isn’t closed within the first six days you keep the interest earned with no penalties

Our Verdict

Interest rates on savings accounts are on the increase, the best high yield savings accounts are currently offering 1.30% so this CD is slightly better at 1.5% for deposits of $25,000. My recommendation is to focus on the rewards accounts that offer up to 5% APY instead. Also as noted in the comments you must withdraw the full amount from the CD, no partial withdrawals.

Hat tip to @FiSnowball