We asked on Twitter which cards readers want to see a review on, and a lot of people were interested in seeing more on the Bank of America Travel Rewards card, so here goes.

Contents

Card Overview

Link to Bank of America Travel Rewards

- No annual fee

- No foreign transaction fee (Bank of America cards are chip-and-pin enabled)

- Card earns 1.5x everywhere with no maximum earnings

- Earn a bonus if you are a Bank of America relationship customer (more on that below)

- Runs on the Visa network and will/can be a Visa Signature card

Like all Bank of America cards, this will come with a free Transunion FICO score and free virtual account numbers for online shopping. The card will also give you access to Bank Amerideals (this is only important if you don’t already have a BofA credit or debit card).

Signup Bonus

- Get 20,000 points after spending $1,000 within 90 days

- The 20,000 points can be redeemed for a $200 statement credit to offset a travel purchase, see Using Points (below)

The signup bonus has been 20,000 for a while and was never higher.

Note, the Preferred customer bonus (see below) does not apply to the signup bonus on the Travel Rewards card, only on ordinary rewards from purchases. (Cash Rewards cards do get the Preferred customer bonus, but not the travel points card.)

Preferred Rewards

To understand the value proposition of this card, it’s important to examine the Bank of America Preferred Rewards program. We’ve reviewed it at length before, and we’ll recap the main points here.

If you have assets held in Bank of America accounts, you are eligible for a bonus as a Preferred Rewards relationship client. Here are the various tiers, along with their earning on this Travel Rewards card:

- Bank of America checking account holders with between $.01 – $19,999: gets a 10% bonus on rewards bringing the 1.5x to 1.65x everywhere

- Preferred Rewards Gold $20,000 – $50,000: gets a 25% bonus on rewards bringing the 1.5x to 1.875x everywhere

- Preferred Rewards Platinum $50,000-$100,000: gets 50% bonus on rewards bringing the 1.5x to 2.25x everywhere

- Preferred Rewards Platinum Honors $100,000+: gets 75% bonus on rewards bringing the 1.5x to 2.625x everywhere

Aside from the credit card bonuses, you also get other benefits by being a relationship client of BofA, such as free trades and discounted fees.

$100,000 is certainly a hurdle, the good news is that the assets don’t need to be held in a checking account to give status; even stock holdings count. Merrill Edge is owned by Bank of America, and any assets held there count toward your Preferred Rewards status. You can have no money in your BofA checking account and still get Preferred Rewards status.

Even those who engage is ‘passive investing’ can use Merrill Edge. For example, you can buy shares on VTI in your Merrill account. Many people can make themselves eligible for the relationship bonus by moving over their retirement account or other brokerage holdings to Merrill Edge.

There’s a good FQF post about the nitty-gritty details of how the $100k requirement works and plays out. It’s based on a three month average; you won’t get status immediately.

Earning Points

Card earns 1.5x everywhere with no cap. Where it gets interesting is if you have Preferred Rewards status. As explained above, you’ll earn 1.65x – 2.625x everywhere depending on your relationship status. 2.6x everywhere is an excellent earning rate for regular, non-bonused spend.

Other Ways to Earn

You can also book travel through their portal and an extra 1.5x per dollar (3x total). This is similar to many online booking agency (e.g. Orbitz or booking.com) which are available on shopping portals to earn extra rewards. Note, you won’t get the relationship bonus on the travel bonus, only on the base earnings. (page 3)

They used to have a shopping portal as well, but that was discontinued a couple of years ago.

Using Points

On a basic level, points are worth 1¢ per point when redeemed against travel charges of $25 or more. For example, if you spent $26.87 on Uber, you should be able to redeem 2,687 points toward that charge and get a $26.87 statement credit.

You might be familiar with the Barclay Arrival which uses a similar system. From what I’ve heard, the Travel Rewards has an even broader definition of travel than most other cards, and considers a wide variety of travel purchases as eligible for redemption.

Now, let’s dive a little deeper.

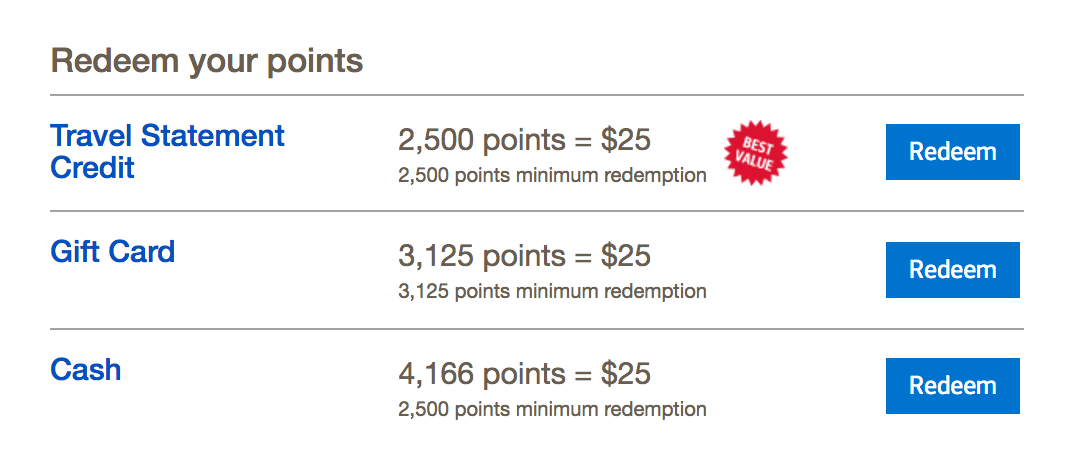

Redeeming Points

Points can be redeemed as a travel credit, cash, or gift card. All redemptions have a minimum of $25.

The easiest would be cash, but that only gets you .6 cents per point. You can do a little better by redeeming for gift cards at .8 cents per point. The recommended redemption is to redeem for travel purchases which gets you a full one cent-per-point.

Some details on how travel redemptions work:

- Points don’t expire, but you can only redeem against travel charges from the past 12 months.

- Total redemption must be more than $25. You can redeem against charges under $25 so long as the total redemption is $25. For example, if you have a $3 bus fare and a $22 Uber, you can redeem them since the total is $25.

- You can redeem part of a large charge. For example, if you have 2,500 point, you can redeem for a $25 credit to offset part of a $$128 airfare charge. And you won’t lose the unredeemed part of that travel charge: you’ll still be able to create another redemption against the remaining $103 from that airfare charge.

A few things to keep in mind as a backup in case you find it difficult to redeem points for travel (e.g. if you don’t travel):

- Things like bus passes, Uber, and tolls (e.g. EZ-Pass) might count as travel and can be redeemed if you have a charge of $25 or more. See list of eligible Merchant Category Codes here on page 6.

- If you have a friend who travels a lot, see if you can transfer your points over to them to redeem and have them reimburse you.

- At the time of this writing, I noticed that numerous gift cards are on sale and can be redeemed at 1 cent per point. Check your account to see if there’s anything you find useful.

- If you are into gift card reselling, you should be able to use the Travel Rewards card to buy travel gift cards (e.g. Southwest or Delta) to trigger the travel credit at 1 cent per point. Then sell those, hopefully without losing too much in the process. This method obviously takes away from getting the full 1% value, but should be better than the .6% cash redemption value and could be better than the .8% gift card redemption value.

Transferring Points

The Travel Rewards card earns points which are part of the WorldPoints program (they seem to have rebranded and don’t call it WorldPoints anymore). Points earned on the card can either be redeemed directly for a travel credit or transferred to another World Points card and redeemed there.

![]()

History: Transferring used to be useful when WorldPoints were able to be redeemed for travel at a higher rate, something no longer available. The 2% Fidelity card used to earn WorldPoints back when it was administered by Bank of America, but that’s no longer the case now that it’s a U.S. Bank card.

Going forward: The main usefulness of transferring points is to transfer over to your Premium Rewards card (or a friend’s card) which will then enable you to cash out the points without dealing with travel at all. Another use of transferring could be to transfer to a friend’s Travel Rewards card who has a travel charge to redeem against.

What Counts as Travel

If anyone has specific data points on which charges do and don’t work for travel redemptions, please let us know in the comments.

Codes as Travel to be redeemed:

- Metro card and bus passes in NYC (1)

- Some data points from a reader: gym membership worked for them, entry fees for 5k races, some museum and historic homes code as Travel while others code as gift shops. And car rentals, motels, cruises, etc. have always coded as travel without any problems.

Does not code as Travel to be redeemed:

- E-Z Pass in Maryland (1)

Final Thoughts

The most interesting part of the card is undoubtedly the 2.625x everywhere without any limits which is really best-in-class. Obviously, it requires having a huge $100,000 relationship with Bank of America, but that’s within reach of a lot of people whether it’s from an IRA account or other stock holdings. Even with the $50k tier, the card earns 2.25x everywhere which is very good.

Another perk of the card is no foreign transaction fees which is uncommon among no-annual-fee cards.

Overall, it’s a card worth considering if you have relationship status with Bank of America. If you are holding funds elsewhere, it can make sense to move funds over to Merrill Edge to qualify, just please consider two things first:

- Ensure that you aren’t losing under Merrill Edge compared to your previous brokerage institution

- Keep in mind that some people can get similar value from other cards. For example, there are a couple of 2.5% cards out there now which is close to the 2.6x that BofA gets. Also, some people value the 1.5x that Freedom Unlimited gives them or the 2x that Blue for Business Plus gives them as being worth that amount.

When considering this card, it’s important to compare it against the Bank of America Premium Rewards Credit Card which is very similar except that it comes with a $95 annual fee and has the following benefits: $100 airline incidental credit, higher earning on dining and travel, and the ability to cash out points directly without dealing with travel charges, among other perks. See our full review of that card here.