Terms on the Chase website state that beginning May 21, 2017, the $300 annual travel credit will be based on the cardmember year, not the calendar year.

As we know, Chase and most premium cards (CSR, Amex Platinum, Amex PRG, Citi Prestige) base their annual credits on the calendar year, not cardmember year. This is golden for signup bonus chasers since we get the credit twice within the first year, effectively creating two signup bonuses on these cards. (In the case of Chase, the year – for this purpose – ends with the date that the December billing statement is generated.)

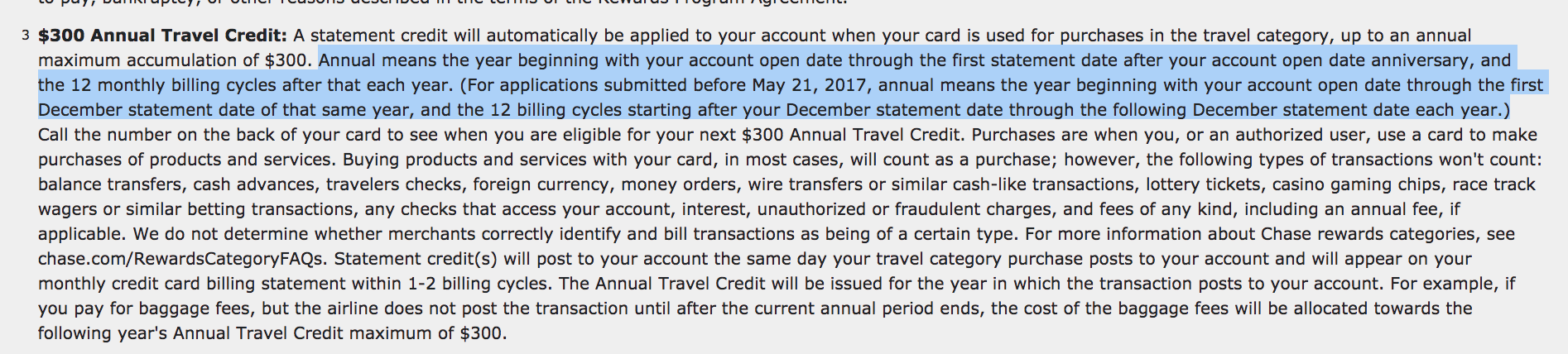

One place on the Chase website now states that for applications submitted on May 21 and beyond, the travel credit will go based on the cardmember year, not the calendar year. This was only recently updated within the past couple of days, and other places on the Chase site have not yet been updated.

Obviously, this is terrible news, but I honestly never understood why they all don’t do this. It’s such a simple money-saver that doesn’t look any worse on paper. Unclear if Chase got the ‘idea’ from US Bank Altitude or it’s just a coincidence.

It’s still possible to get the airline credit twice by squeezing $300 in at the beginning of the second cardmember year and then cancelling the card within 30-days of when the fee hit. But it certainly makes it harder, and most ‘normal’ people won’t do that.

Related: What Counts For The $300 Chase Sapphire Reserve Travel Credit?

FAQ

Will the change affect existing cardholders?

Those who already have the card or who apply through May 20 will be able to get two travel credits in their first year.

Will the change take effect for existing cardholders?

It’s not clear at this time if Chase will change the terms over for existing cardholders as well. Not that it makes much a difference (in the first year you’ll get two airline credits and in subsequent years you’ll get one, in any case), but it is important to know the exact dates to take advantage of the credit.

I’m sure Chase will send out a mailer if/when the system of dates changes on the card. If they do change it for existing cardmembers, it could create a one-time opportunity to get another extra $300 credit out of this. More likely, this won’t happen.

Should I apply for the card now?

Hopefully, if you are eligible, you already applied when the bonus was 100k. That said, if someone is on the fence to apply now (e.g. just got out of 5/24, just started churning, whatever), I think it makes sense to apply now before May 21 with the 50k bonus, and not wait with the hopes that the bonus will increase again to 100k.

Credit goes to Travelafterwork for picking up on this change