Update 12/29/20: Rate is now 2.5% (was 3%)

Offer at a glance

- Interest Rate: 2.5%

- Minimum Balance: None

- Maximum Balance: $10,000

- Availability: If you don’t live within state, select “Not Listed – Let Us Help”, you’ll then need to make a $5 donation to join.

- Direct deposit required: Yes, must be above $500 per month to get reward rate

- Additional requirements: Yes, see below

- Hard/soft pull: Hard

- Credit card funding: None

- Monthly fees: None

- Early Account Termination Fee: $25 if closed within 180 days

- Insured: NCUA (60238)

The Offer

- Receive an increased APY of 3% on up to $10,000 in deposits from Great Lakes Credit Union when you complete the following requirements:

- Make 15 debit card purchases totaling $150 or more

- Receive direct deposits totaling $500 or more

- Enroll and receive eStatements

- Pay one bill per month via Bill Pay or login to mobile banking once per month

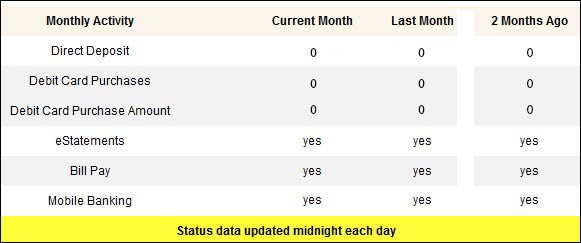

Requirement counter at the bottom of the summary page that updates daily on what requirements you have and haven’t met.

Avoiding Fees

This account has a $5 monthly fee if you don’t receive a direct deposit above $500 or you complete less than 5 debit card purchases (no Returns, PIN or ATM). There is also an early account termination fee of $25 if you closed your account within 180 days.

Rate History

- 2012 – October 2013: 4%

- October 2013 – Current: 3%

- Note: On 4/1/18 the requirements were changed (monthly debit spend requirement increased to $150 from $100. Number of transactions increased to 15 from 10

Our Verdict

I don’t like the GLCU rewards checking account that much for a few reasons:

- It’s a hard pull to open

- Debit card transactions need to total $100 per month

- You cannot fund with a credit card

Let’s assume you’d use a credit card that earned at least 2% cash back on your debit card transactions, you’re losing out on $24 per year in that alone. Instead of opening this account and being charged a hard pull, you could open a credit card with a cash sign up bonus instead and receive $200.

Let’s assume you deposit the full $10,000, you’d be earning $300 per year compared to $100 if you were using a checking account with a 1% APY. Personally I don’t think that justifies the hard pull and debit card requirements. I prefer two other checking accounts for different reasons:

- Mango Money, because it offers a 6% APR without a hard pull (and $20 direct deposit bonus). Although this is really a 5.14% APR when you take into account the monthly fees, assuming you have the maximum $10,000 deposited.

- Lake Michigan Credit Union, because you can fund $5,000 with a credit card which can be useful for meeting minimum spend requirements and it has a 3% APR, but you can have up to $15,000 deposited at a time. Plus you only need to make 10 debit card transactions and there is no minimum amount specified.

It used to be possible to open multiple rewards checking accounts with GLCU, this loophole was closed in July of 2014. Because of all these reasons, I wouldn’t recommend signing up for this rewards checking account at the moment.

If you know of any good nationwide rewards checking accounts, please let me know in the comments below and I’ll add them to the site. I’ve been investigating Kasasa accounts recently, so they are next on the list. We recently asked our readers what blogpost or tool they wished existed and didn’t, reader Liz wanted more information on rewards checking accounts which is why we’ll be posting about these more often. Liz will receive a $5 Amazon gift card for her troubles, feel free to make your own suggestion on that post and you could receive one too!

Ended up closing this account a few months ago via phone. They mailed a check for the small balance I had in checking as well as the $5 in savings. When asked why, I told them that their interest rate is no longer competitive. I can leave my $$ in excess of their $10k limit at online savings accounts paying between 3-4% with out the “work” of debits and DD. It’s been dormant for over a year, hoping they would raise their rates. Lake Michigan CU might be next for the same reason.

Has anyone NOT gotten paid interest for November? According to the free checking status, I met all requirements (spend, DD, etc). I’ve sent messages and tried calling but no one has gotten back to me. Thanks.

Highly discourage opening an account with these folks, GLCU. I did a CD promo with them and when I tried to close accounts after the promo, all hell broke loose-they sent me check for over amount that was left in account, i didn’t cash it and let them know of error, had terrible time communicating with them, being on hold and tossed around to different departments (multiple weekly calls), they ended up putting something on my credit report (yes for a CD/checking – only accts I had with them) claiming I hadn’t paid a debt in months. Took me well over a YEAR, to get this straightened out-Buyer Beware.

15 DC requirement totaling $150 per month is bad…..it is too much for $250 per year!! Not worth it, IMO

Are any of you still using this account? If so, has any ACH transfer been working to trigger the DD requirement?

I quit using the account and closed it. Yes, any ACH transfer works to trigger the DD. There is a tracker on their website, so you’ll know right away if something worked.

I like when sites have that tracker. Did you quit because they lowered the rate to 2.5% or some other reason?

They lowered the rate and I wanted to close some accounts at various banks because I felt I had too many.

This is only 2.5% now.

Can you update the post with the 2.5% rate?

Link needs to be updated William Charles

William Charles

https://www.glcu.org/bank/checking/free-checking/

Updated, thanks

new account is now 2.5% not 3%

any word on existing accounts?

My account has been open since November 2018 (spreadsheets are nice)

August 2020 interest paid 2.5%

Not as good as it used to be, I’m migrating finances again.

This looks like a No- GO checking account.

From the fee schedule it appears that this applies to the Savings account, not the checking account.

Per their fee schedule:

Savings Only Membership….. $5.00 per month unless each month you maintain a $500.00 direct deposit, a $500.00 average daily balance, OR an additional GLCU deposit or loan product.

If you don’t meet the requirements you just don’t get the 3%. I couldn’t find where you’d be charged a fee if you don’t do the full requirements.

here is the link: https://www.glcu.org/bank/checking/free-checking/