Update 1/5/2021: for anyone still doing this: reader Sexy_kitten7 notes that you no longer earn interest above $1,000, even on funds which were originally earned as interest (previously, only external loaded funds were subject to the $1,000 limit).

[Originally posted on 6/1/16, reposting on 7/1/16 since change is now going into effect and is also showing on the Netspend site. Time to unload our Netspend accounts now…]

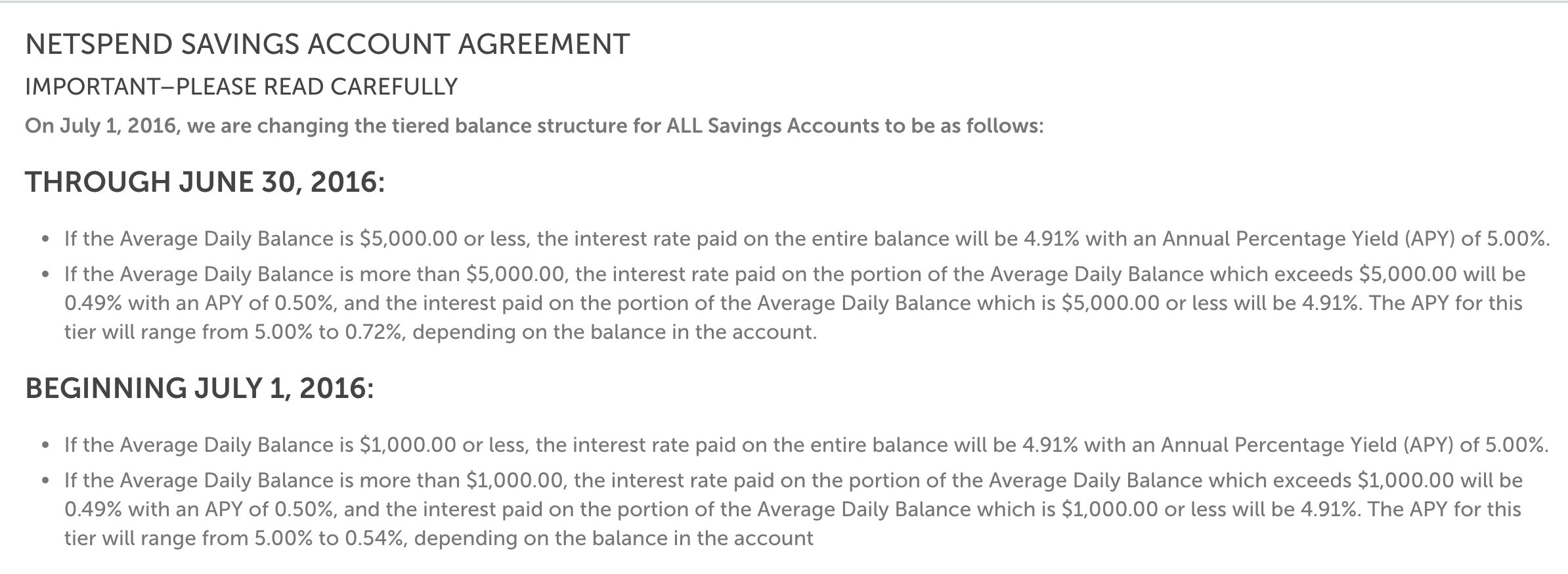

Netspend is lowering the amount that earns a 5% APY rate on all of their prepaid cards from $5,000 to $1,000. The change will take effect on July 1, 2016, and it applies to all Netspend cards, including Netspend, Brinks, Western Union, HEB, Control, Ace Elite, and the Paypal Prepaid too.

You can find this update in your Netspend login by going to Move Money > Savings > Savings Terms and Conditions.

While you can keep the accounts for the $1,000 in interest, it’s probably not worth the effort, especially since there is already a slight hassle with keeping it fee-free from the 90-day inactivity fee.

There are still numerous other options which earn above-average interest rates, including Consumer’s Credit Union which earns 4.59% on up to $20,000, and the Mango and Insight prepaid cards. See “Which High-Interest Savings Account Should I Get?” for a run-down of all the options for high-interest accounts and for the best standard rates as well.

How to Unload

On July 1, most of us will want to empty out the balances from the accounts. Interest is paid quarterly so we’ll get a final interest payment for April – June, and we’ll then empty the accounts.

All the Netspend accounts come with an account/routing numbers and are ACH-enabled. Using the account/routing numbers, you should be able to pull the money out into your linked bank account or you can pay your credit card bill on the card issuer’s website. Be sure to first transfer the money from the savings account into the prepaid before making the ACH transfer.

Even savings accounts are getting killed off. 2016 has been brutal.

Hat tip to tbradnc on Reddit

Update 7/1/16: I’ve been having success pulling out money via ACH transfer to my regular checking account; I’ve so far kept my pulls under $2k each so as not to raise any red flags.