Update 1/8/24: Increased to 5.01%

Update 12/13/22: Increased to 4.1%

Update 10/30/22: Increased to 3.50%

Update 9/20/19: Rate decreased to 2.01%.

Update 8/21/19: Rate decreased to 2.20%.

Update 8/7/19: Rate decreased to 2.35%.

Update 6/2/19: Rate increased to 2.51%, hat tip to reader bbbb.

Update: Rate increased to 2.3% APY on 1/19/19.

Originally posted 3/19/18. Reposting 7/4/18 since rate increased from 1.85% to 2.05% putting them at the top of the market, currently.

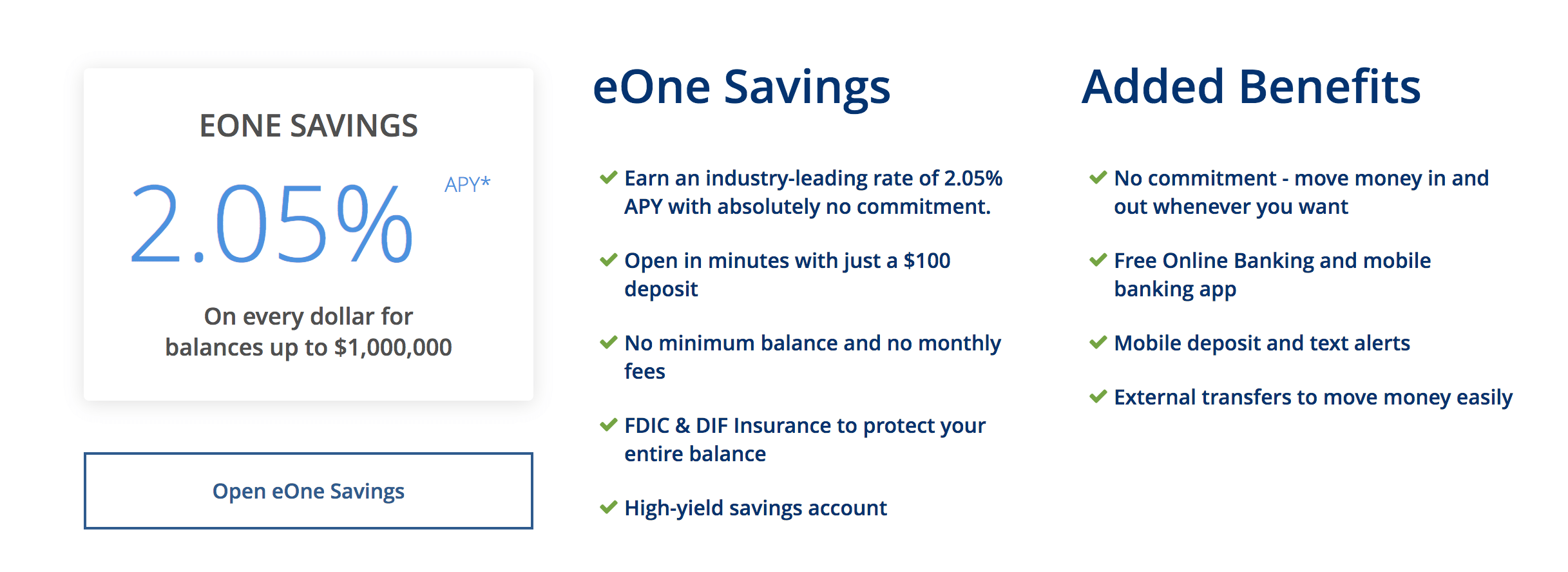

Offer at a glance

- Interest Rate:

1.85%2.05% APY - Minimum Balance: None, $100 minimum opening balance

- Maximum Balance: $1,000,000

- Availability: Nationwide

- Hard/soft pull: Hard (all datapoints are quite old though). Recent datapoint says soft

- ChexSystems: Yes

- Credit card funding: None

- Monthly fees: None

- Insured: FDIC up to $250,000

The Offer

- Salem Five Direct is offering

1.85%2.05% APY on balances up to $1,000,000 with their eOne Savings account

Avoiding Fees

This account has no monthly fees to worry about

Our Verdict

This is currently the highest APY savings account with no requirements. Accounts with requirements earn up to 5%. An account like this is more suited to somebody who just wants to set and forget their money, or has so much in cash that they can’t manage enough rewards checking accounts (these all have caps anywhere from $1,000-$20,000+). It looks like this account does have a hard pull, or at least Salem Five used to do a hard pull. I’d like to see some newer data points on that if I’m honest. Either way it’s nice to see deposit accounts continue to offer higher and higher APYs and this might be an account worth considering for some people.

Readers point out in the comments that it looks like Salem Five Direct does not automatically raise rates for existing account holders and you have to call in to get the higher rates. I hate this practice as it removes the set and forget factor that is attractive on basic savings accounts.

Please feel free to share your own experiences with Salem Five Direct in the comments below.

They’re showing a 12 month CD for (5.41%) 5.55%. Minimum to open is $10K though.

https://www.salemfivedirect.com/current-offered-rates/

This is over 5%

eOne Savings earns 5.01% APY (Annual Percentage Yield) on daily balances of $0.01-$1,000,000

6 month CD rate is 5%, lower than savings?

can confirm as of May 11th 2022 they hard pulled my equifax report when i opened a checking account with them.

Current rate is at 5.01%

https://www.salemfivedirect.com/#eonesavings

SalemFive eOne savings at 4.1%

https://www.salemfivedirect.com/#eonesavings

I need to check on this, but I read a post here that existing accounts do not increase automatically. You have to contact them to request it.

I also see this text on the page linked above: “The stated APY applies to new eOne accounts opened as of today’s date. “

Two points:

Their CS seems to be in the US. You can tell by the words used by their Secure Chat agents (when it works). I couldn’t get it to work at all in one browser and only spotty using their Mobile version. Worked fine in a different browser. Agents may be using more than one screen at a time and dealing with more than one customer though since there were delays for responses.

Their transaction Alerts are prompt and detailed. Another bank I’m trying only has limited alerts and none for deposits or withdrawls.

Not impressed so far. Taking far too long to get set up with full access and funded.

And there is NO indication at all of pending status of funds. Nothing is appearing.

Rate now at 3.5% and is listed on the High Yield Savings page. Not updated for new information here though.

@chuck William Charles

William Charles

Opened one to try it out. Doesn’t seem my information will be fully operational until tomorrow though … business day

Updated

Rate dropped to 0.80% as of August 13, 2020