Update 7/27/19: More people are seeing this offer

Update 1/21/19: Lot more people seeing this offer again.

Update 08/15/18: Reposting as lots of reports of readers seeing this offer again.

Update 05/21/18: Reposting as this is showing up for people again frequently.

Update: It’s actually possible to get the 25,000 offer with the 0% APY/no BT fee when using incognito mode.

The Offer

You must use the incognito mode trick to get the 25,000 offer. More on that here.

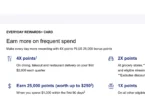

- American Express is offering a new bonus on the Amex EveryDay card:

- Earn 25,000 points after you spend $2,000 or more within the first three months

- Receive a 0% introductory APR on purchases and balance transfers for 15 months, then a variable APR of 14.24% to 25.24%

- No balance transfer fee for first 60 days

Card Details

- No annual fee

- If you’ve hard this card before, you’re not eligible for the sign up bonus on this card

- 2x points at US supermarkets, on up to $6,000 per year in purchases (then 1x); 1x points on other purchases

- Use your Card 20 or more times on purchases in a billing period and get 20% more points on those purchases less returns and credits

- You cannot get the bonus on the cards if you’ve ever had the card before

Our Verdict

Update: Now that this offer is 25,000 points + 0% introductory APR and no BT fee it’s definitely worth doing. 25,000 points is the highest bonus we’ve seen on this card, so the 0% APR no BT fee is just an added bonus. This is definitely going on our best credit card bonus page.

It’s currently possible to get a bonus of 25,000 points after $2,000 in spend within three months on this card by using the incognito mode methods. Obviously this offer is 15,000 points less but does come with the 0% APR no BT fee offer. I think most people will be better off with the higher points offer, but if you need to float money or are trying to pay down credit card debt then this offer could make sense.

It’s interesting to see American Express enter this 0% APR no BT space and this is actually the best offer of this type in the market (Chase offers the same with the Chase Slate, as does Bank of America with the BankAmericard Credit Card but neither come with any points sign up bonus). Citi have previously stated that they were exiting the competitive rewards space to focus on these types of offers, so they won’t be happy with this change of direction. I suspect we will see more of these types of offers to come as interest rates rise.

As always before applying for this card, I’d strongly recommend you read these things everybody should know about American Express credit cards. It includes things such as the reconsideration number to call if your application is denied.

Hat tip to DDG