Update 10/20/20: SavorOne signup bonus increased to $200.

Update 5/7/20: Signup bonus on Savor is $300, currently. Annual fee still not waived for the first year.

Update 7/9/19: They no longer waive the $95 annual fee first year on the Savor One card. There is an increased offer showing for $400 for some people (I see it in my regular browser; incognito shows $300 for me, fee not waived either), so it’s basically a wash with the extra $100 and extra $95 fee. (ht SMan) Updated below.

[Update 5/22/19: Signup bonus reduced from $500 to $300.]

Capital One launched the Savor card in October, and today the bank announced an enhancement of the Savor card with 4% on dining & entertainment and a $500 signup bonus. They also announced a brand new no-fee SavorOne credit card.

Capital One Savor

The Savor card comes with the following signup bonus:

- Get $300 when you spend $3,000 within three months from account opening.

- They’ve also added a new benefit for 2019 to get reimbursed a $9.99 monthly Postmates Unlimited subscription cost.

Card earns the following rewards rates with no earnings limit, no minimum redemption, and no rewards expiration:

- 4% cashback on dining, entertainment, and popular streaming services

- 3% cashback on groceries

- 1% cashback everywhere else

- They’ve added a benefit to get 8% cash back at Vivid Seats

Card Details:

- $95 annual fee (not waived the first year)

- No foreign transaction fees, like all other Capital One cards

- Access to premium experiences in dining, entertainment and more

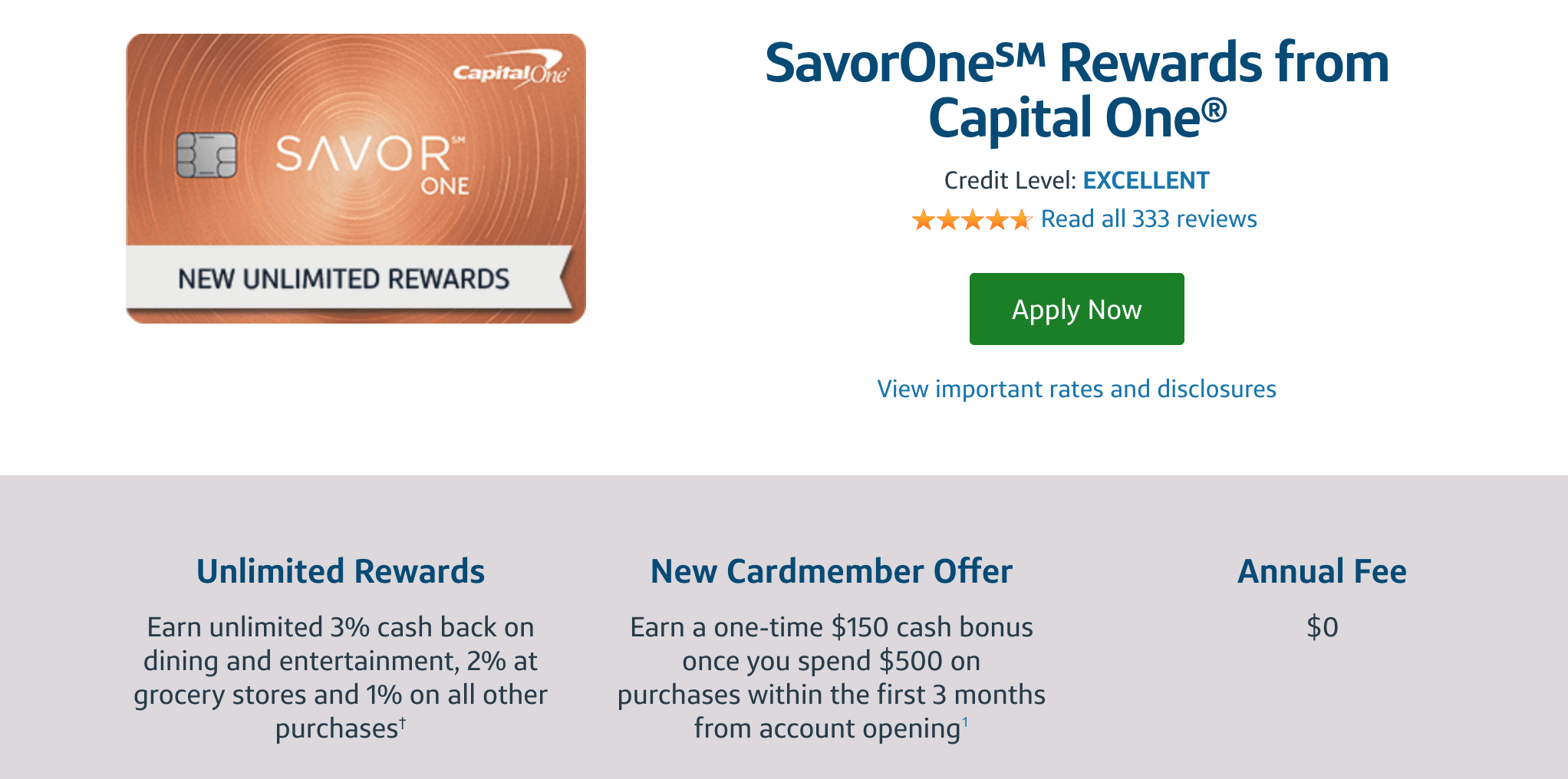

Capital One SavorOne

The SavorOne card comes with the following signup bonus:

- Get

$150$200 when you spend $500 within three months from account opening.

Card earns the following rewards rates with no earnings limit, no minimum redemption, and no rewards expiration:

- 3% cashback on dining, entertainment, popular streaming services

- 2% cashback on groceries

- 1% cashback everywhere else

Card Details:

- No annual fee

- No foreign transaction fees, like all other Capital One cards

The Fine Print

What counts as dining? Purchases at restaurants, cafes, bars, lounges, fast-food chains and bakeries.

What counts as entertainment? Buying tickets to a movie, play, concert, sporting event, tourist attraction, theme park, aquarium, zoo, dance club, pool hall or bowling alley. Also, making purchases at record store and video rental locations. This excludes non-industry entertainment merchant codes like cable, digital streaming, and subscription services.

Our Verdict

Basically, you get 4% instead on dining and entertainment for the $95 annual fee instead of 3% with the no-fee card. You’ll have to spend $9,500 per year to justify that cost on a purely rewards-basis analysis.

The $500 cash signup bonus on the Savor is sweet! And 4% cashback on dining and entertainment is good, though if you have a premium card like the Chase Sapphire Reserve you can end up with better value there with their 3x earnings on dining (depending how you redeem those points). If not, it could make sense for someone who spends heavily on dining and entertainment. The Barclay Uber card also offers 4% on dining.

Check out these Things to Know about Capital One Credit Cards before applying. People often get denied by Capital One for various reasons; maybe we’ll get lucky and they’ll go easy on Savor applications.

As per our communication with the bank, existing Savor cardholders will get upgraded to the 4% dining and entertainment rate, and they’ll be grandfathered in with no annual fee (the bank is considering the Savor card as part of the existing line with an upgrade, and the SavorOne is the new product). Capital One has sent out a mailer to cardholders with this information as well.

We’ll also add the Savor to our list of Best Current Credit Card Signup Bonuses, list of Best Cash Credit Card Signup Bonuses, and list of Best Credit Cards For Restaurant Spend.