Update 11/3/24: Rate reduced to 4%

Update 9/27/23: Interest rate has been increased to 5% again.

Update 2/2/20: Interest rate has been reduced to a maximum of 3%

Reposting 5/8/18 since interest rate went up from 3% to 4% (HT: Luke).

Offer at a glance

- Interest Rate: Max of 4%

3%APY - Minimum Balance: None

- Maximum Balance: None ($2,000 for top rate)

- Availability: Nationwide with $5 donation

- Direct deposit required: No

- Additional requirements: No

- Hard/soft pull: Mixed datapoints

- ChexSystems: Yes

- Credit card funding:

Up to $1,500 with Visa or MastercardNo longer offers credit card funding - Monthly fees: None

- Insured: NCUA

The Offer

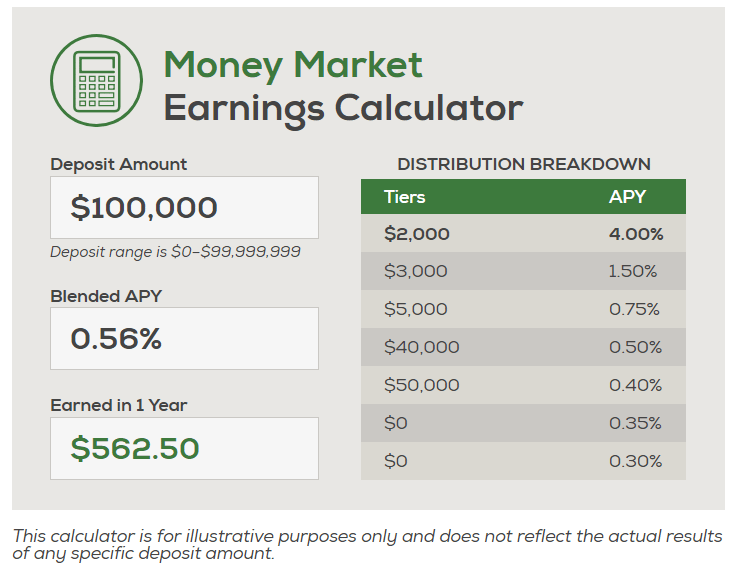

- Premiers Credit Union offer a money market account with a reverse tiered interest rate (the more you have in the account, the lower APY you receive). The tiers are as follows:

- $0-$2,000: 4%

3%APY - $2,000-$5,000: 1.5% APY

- $5,000-$10,000: 0.75% APY

- Rates continue to decline

- $0-$2,000: 4%

This means the first $2,000 in the account will earn 4% APY, the next $3,000 will earn 1.5% APY etc.

Referral Bonus

You can also get a $50 bonus for signing up using a referral link. The person who refers you will also get a $50 bonus (up to $1,000). Reader Luke told us about this bonus and also that the account was a soft pull, his link can be found here. Feel free to share your own links in this linked post. DO NOT SHARE THEM IN THE COMMENTS BELOW!

The Fine Print

- No minimum deposit required to open an account.

- Limit one Money Market Account per social security number.

- Federal Regulation D states that you may make no more than six (6) automatic or preauthorized transfers from your share savings or money market account per calendar month.

- Certain withdrawal limits apply to Money Market Accounts, be sure to review your Membership and Account Agreement Disclosure for details.

- All bank account bonuses are treated as income/interest and as such you have to pay taxes on them

Avoiding Fees

This account does not have any monthly fees to worry about. Unsure if there is any early account termination fee or not

Becoming A Member

There are a number of ways to join for free (but most people won’t be eligible). In addition anybody can join by making at least a $5 donation to Impact on Education (they will also match your donation).

Our Verdict

Problem with this account is only the 4% is interesting (and even the 1.5% isn’t that interesting). It’s nice that there are no requirements, but for most people it simply won’t be worth opening a new account for. If you max out the 4% then you’re only getting $80 annually in interest (and that doesn’t even include the opportunity cost of putting that money into another high interest account). I think most people would be better off opening another account for a bank account bonus instead.

You can view a full list of accounts with high APY’s available here. The other thing to mention is that this account is also relatively new (started January, 2017) so there is no guarantees this rate will stick around long term.

Hat tip to reader John S