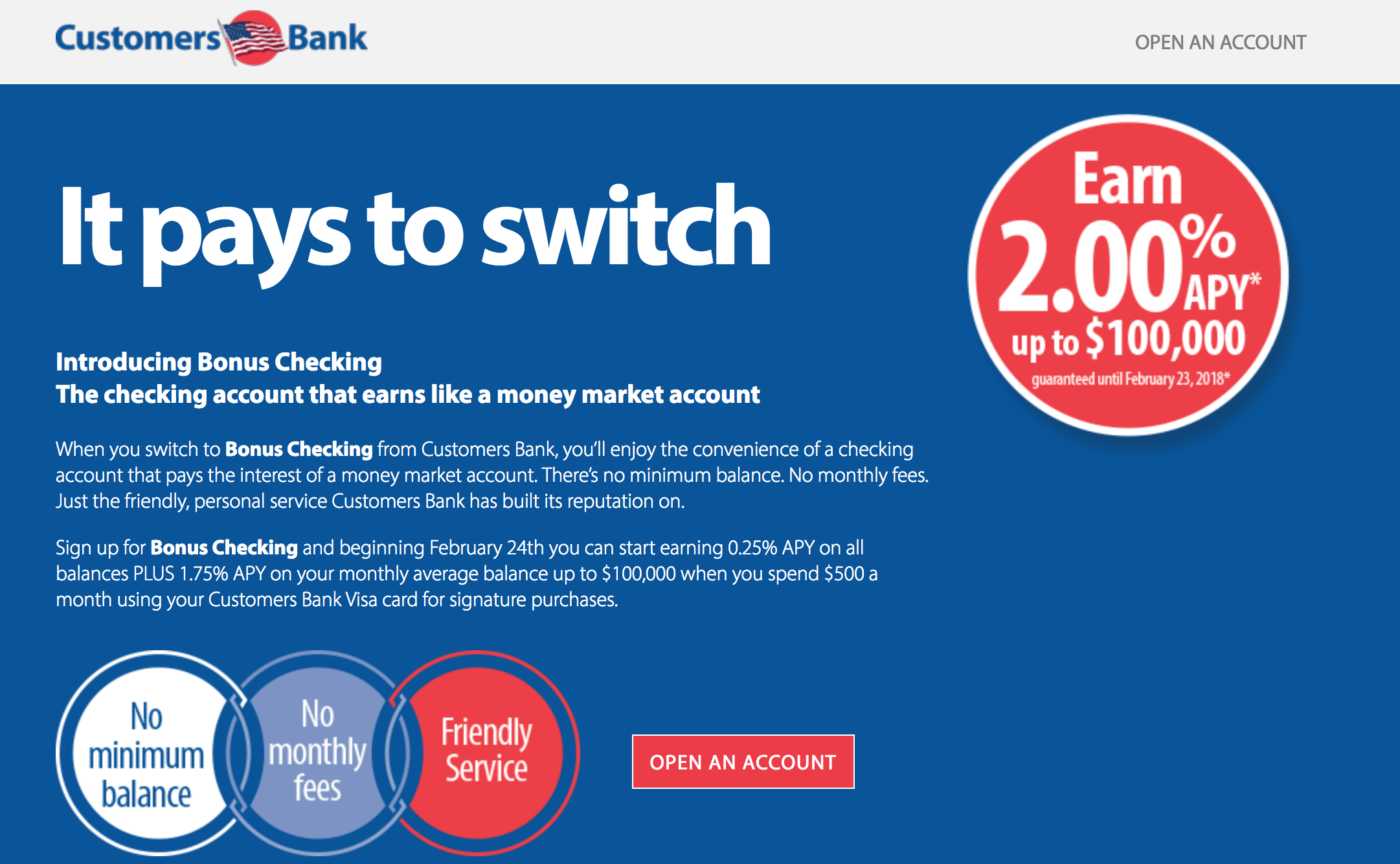

Offer at a glance

- Interest Rate: 2.00% APY

- Minimum Balance: $0.01 (minimum opening balance is $10)

- Maximum Balance: $100,000

- Availability: Nationwide

- Hard/soft pull: Unknown

- ChexSystems: Yes

- Credit card funding: None

- Monthly fees: None

- Insured: FDIC

The Offer

- Customers Bank offers a 2% APY checking account on balances up to $100,000 when you spend at least $500 in signature debit card transactions

The rate is comprised of a base rate of .25% APY, plus a bonus 1.75% APY when meeting the debit card requirement. Customers Bank is located in the Northeast, but seems to be available for all US citizens to open an account.

The Fine Print

- Annual Percentage Yield (APY) as of 12/13/2017

- To be eligible to open this account, new money is required (funds not currently on deposit with Customers Bank)

- APY of 2.00% will be guaranteed on all balances through February 23, 2018. As of February 24, 2018 all balances will earn 0.25%APY and the additional bonus APY of 1.75% will only be earned when the Visa Debit Card signature based purchases equal $500 or more during the statement cycle.

- The “Bonus” APY of 1.75% will be calculated on the average daily balance for the statement cycle and credited on the statement cycle ending date for average daily balances up to $100,000.99.

- During statement cycles when the Visa Debit Card signature purchases do not total $500 or more, the Bonus checking account will earn 0.25% APY.

- Bonus Checking is a variable rate account and the account interest rates and APYs may change after February 23, 2018 without notice

- Limit of one Bonus Checking account per tax identification number

Avoiding Fees

There are no monthly fees on this account.

Our Verdict

Two important things to keep in mind before getting in on this. First, they clearly write the rate can change at any time; I don’t know if this bank has a history of bait-and-switch, for now I’ll give them the benefit of the doubt.

The other thing is, of course, the $500 debit card requirement. They require signature purchases and – to keep it simple – let’s assume you’re losing out on credit card spend when doing so. I’ll figure a 2.5% loss due to the spend, or $150 per year. After figuring that, it’s only a small increase over the top savings rate which is (at time of this writing) ableBanking 1.70% APY. Fully maxing out this Customers account with $100k, you’ll get an extra $300, but lose $150 from the spend, cutting the gain in half. More realistically, you won’t have a full $100k in the account.

Anyway, it’s another interesting option, especially if you have lots of cash reserves, but overall I’m not sure how many people will find this offer worthwhile. We’ll add this to our List of Best High Interest Saving Rates (though it won’t make the Basic list there due to the $500 requirement). You can check out that resource for up-to-date information on the best savings rates available.