Update (11/21/17): As pointed out by readers Dan & Jeff S Northpointe is no longer accepting new applications for this account. I got in contact with Bill Clancy (VP/Deposit Banking at Northpointe) asking if this was permanent and what would happen to existing account holders and he provided the following statement:

Yes, correct – our 5.00% APY Ultimate Checking has been closed to new account holders. This is a permanent decision.

There are no changes at this time to any existing Ultimate Checking accounts. As with any business and any product, we’re continually evaluating our products and services to ensure they continue to meet both the organization’s and its customers’ needs. Our Ultimate Checking falls into this process as do all our other products and services. If or when a change may occur, it will of course be done thoughtfully and with significant consideration for what’s best for the bank, its shareholders and its customers.

Northpointe still offer their UltimateSavings (1.12% APY) & Money Market (1.5% on balances $25,000-$1,000,000) accounts. If you’re in the market for a high interest savings account, we’d strongly recommend reading our dedicated post here.

Offer at a glance

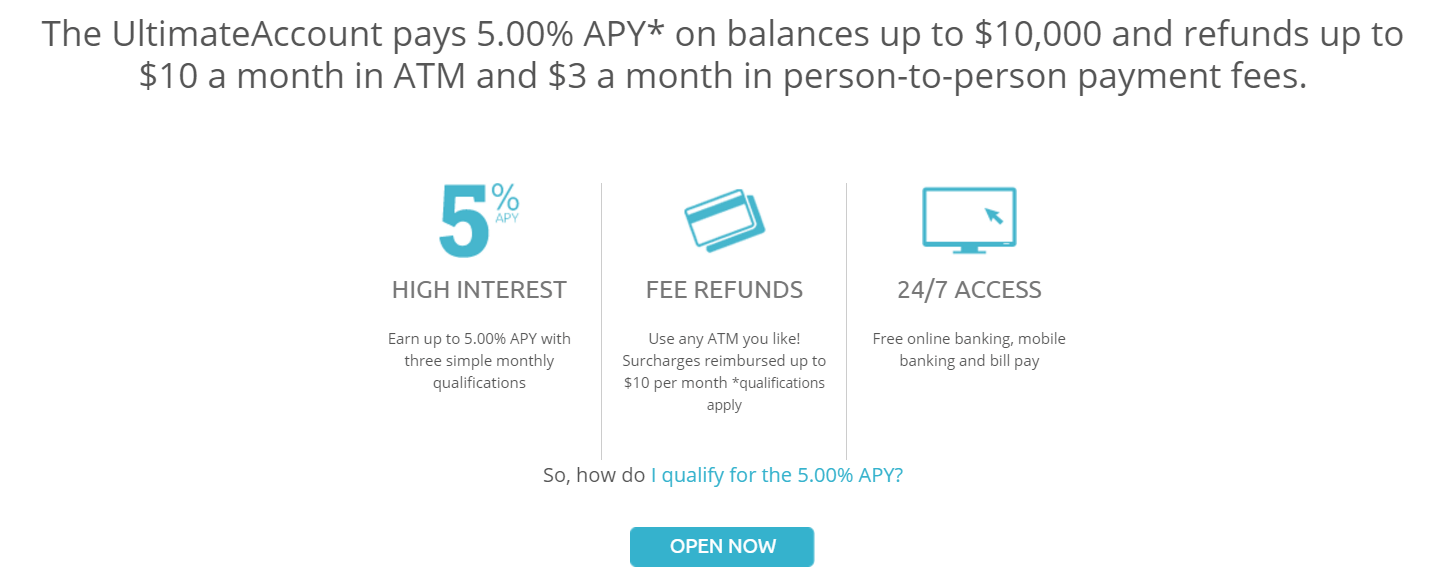

- Interest Rate: 5.00% APY

- Minimum Balance: none ($100 initial deposit)

- Maximum Balance: up to $10,000 (beyond that the rate is .10% APY)

- Availability: Nationwide

- Direct deposit required: No

- Additional requirements: Yes, see below

- Hard/soft pull: Soft

- Credit card funding: Yes, up to $100

- Monthly fees: None

- Household limit: None (one per SSN/ITIN)

- Insured: FDIC

Contents

The Offer

- Open the UltimateAccount checking account at Northpointe Bank and receive an interest rate of 5% APY on balances up to $10,000.

Any portion of the balance which is above $10,000 will earn an interest rate of .10%. (The first $10,000 will still earn the full 5% interest.)

Requirements

There are three requirements necessary in order to be eligible for the 5% interest rate:

- Must enroll in e-statements.

- Must make 15 debit card purchases. (The 15 transactions must post and settle during the statement period to qualify.) More details on this below.

- Must set up an automatic withdrawal or direct deposit of $100 each month.

These requirements must be met based on the statement period, not based on the calendar month. If you don’t meet these three qualifications, then the interest rate is just .05%.

Meeting the Debit Card Requirement

Initially, this account had a 15 transaction + $500 debit requirement; since May 2017, the $500 requirement has been removed and you just need to hit 15 debit purchases of any amount.

That said, Northpointe has added terms indicating that they’ll switch or close any account that isn’t using the debit card in an ordinary manner for things like gas, groceries, and similar. We wrote more about this in a dedicated post.

Meeting the Deposit/Withdrawal Requirement

The direct deposit requirement is pretty typical, but here they gave us more leeway and allowed an automatic withdrawal as well. The main goal here, apparently, is that you should actually use the account and not just park $5000 in it, so they’re okay as long as they see some regular account activity such as a direct deposit or automatic withdrawal of $100.

Based on my correspondence with the bank:

- The $100 withdrawal requirement can be fulfilled, for example, by making a $100 credit card payment, initiated by the credit card.

- Making ACH transfers from another bank account may work in many cases to fulfill the requirement of a direct deposit, but it can vary by the bank as to whether it gets coded as a direct deposit.

Making an ACH withdrawal should probably work in any case since that doesn’t require a special ‘direct deposit’ coding to qualify. Thus, it should work for you to just have an automatic transfer of $100 from your regular checking account to your Northpointe account and another transfer back. Even if the transfer to the Northpointe account would not come up as a ‘direct deposit’, the subsequent withdrawal should presumably be considered an automatic withdrawal and suffice to make you eligible for the 5% interest rate.

Signup Bonus

There isn’t any signup bonus on this account.

At one point there was a $50 or $100 signup bonus offer, but it’s unlikely that will come back. At another point there was a $25 referral bonus offer which gives each party a $25 referral; also unlikely to come back.

The Fine Print

- Rates are subject to change after the account is open.

Funding the Account

The bank requires an initial funding of at least $100. The funding can be done via ACH transfer from your existing checking or savings account or via a credit card.

Avoiding Fees

This checking account does not come with any monthly fees.

The only fee to be aware of is a 12-month dormancy fee of $5 (more details here). If you are using the account for the 5% interest, this won’t apply to you as you’ll have activity when meeting the other criteria, but it’s worth keeping in mind. There is also an early account termination fee of $10 if closed within 120 days.

ATM Fee Waiver

Not only is the account fee-free, they’ll actually reimburse you for up to $10 in ATM fees charged by the ATM owner. (Northpointe themselves will never charge you any ATM fees from their end.)

This is a really nice benefit of having this account as you can always fall back on it to withdraw money at any ATM nationwide (or even internationally, perhaps) and get the fees reimbursed. Since you’ll already have $5000 in the account, you won’t have to worry about making sure the account has funds which you can withdraw.

Our Verdict

Since the account requires ‘ordinary’ debit card usage, it’s not nearly as valuable as a straight 5% APY account. That said, 5% on $10,000 is from the best high-yield options around, and some people will find it worthwhile to use their debit card regularly so as to get the rate.

Check our post on Best High Interest Savings Accounts for other high-yield options.