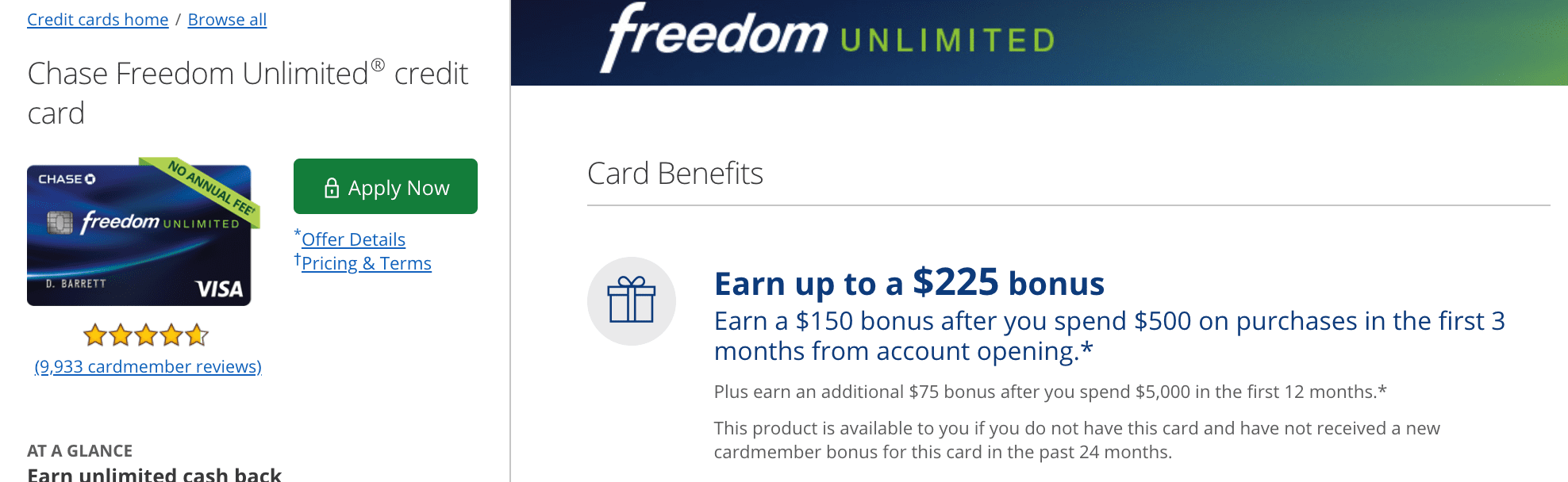

The Offer

- Chase Freedom Unlimited now has a new sign up offer to get up to $225, broken down as follows:

- Get $150 bonus after you spend $500 on purchases within the first three months of card membership.

- Get an additional $50 or $75 bonus after you spend $5,000 on purchases within the first year of card membership. It sometimes shows $50 and sometimes shows $75. Refresh to find the $75 offer.

Card Details

- No annual fee

- Card earns 1.5% cash back on all purchases

- Chase 5/24 rule applies to this card

- Full review

Read: Chase Freedom Vs Chase Freedom Unlimited – Which Card Is Better?]

Our Verdict

Most readers won’t be eligible for this card due to the 5/24 rule. If you are eligible it might make sense to apply for another Chase card instead (e.g Chase Sapphire Preferred or Chase Sapphire Reserve) and then downgrade to this card at a later stage if you value the 1.5x points earning.

Offer is really worse than the $200 offer with $500 spend which became available a couple of months ago since this offer requires $5,000 in spend to get the $225 bonus. That said, if you plan on spending a lot on the card it could make sense. We’ve also seen a bonus of $300 on this card previously as well. As always if you have any questions about Chase, read this post first.

Hat tip to reader boomX