Deal has expired, view the best current checking bonuses by clicking here.

Offer at a glance

- Maximum bonus amount: $150

- Availability: Certain counties in TX, more information here.

- Direct deposit required: Yes, $100+

- Additional requirements:

- Hard/soft pull: Hard pull (although this is an old datapoint and customer service is apparently saying it’s soft)

- ChexSystems: Unknown

- Credit card funding: Can fund up to $250 with a credit card

- Monthly fees:

- Early account termination fee: No early account termination fee

- Household limit:

- Expiration date: December 31st, 2018

Contents

The Offer

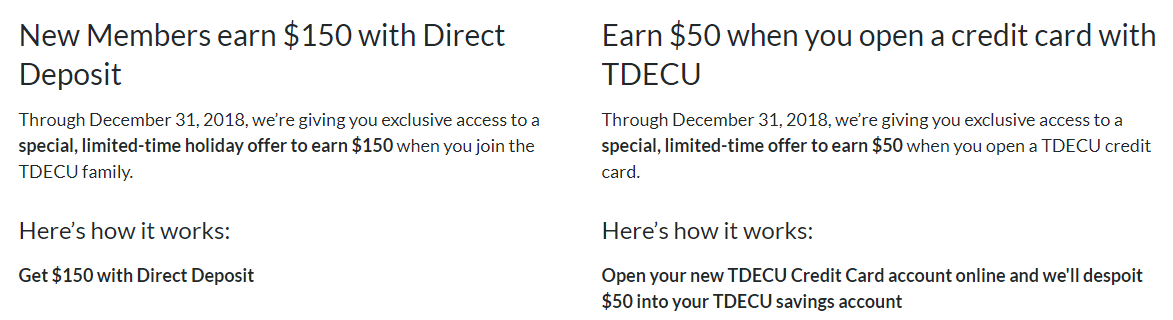

- Open a new TDECU checking account and add a recurring direct deposit of $100 or more and receive $150

- Open a credit card and receive another $50

The Fine Print

- TDECU membership required. Incentive offers good through December 31, 2018, and are considered interest and will be reported on IRS Form 1099-INT.

- Other restrictions may apply; see credit union for details. 1$150 will be deposited into new Member’s SavingsAccount after 60 days of account opening.

Avoiding Fees

Monthly Fees

Classic checking has no monthly fees to worry about

Early Account Termination Fee

There is no early account termination fee

Our Verdict

The credit cards don’t look very exciting, so I’d stick to the checking bonus. An old datapoint says opening the checking account is a soft pull but apparently customer service reps are saying it’s now a soft pull. It’s difficult to determine if this is a good or bad deal until we know for sure if it’s hard or soft. As always please share your data points in the comments below.

Big thanks to reader, Jonathan F & T who let us know. Learn how to find bonuses and contribute to the site here.

Useful posts regarding bank bonuses:

- A Beginners Guide To Bank Account Bonuses

- Bank Account Quick Reference Table (Spreadsheet) (very useful for sorting bonuses by different parameters)

- PSA: Don’t Call The Bank

- Introduction To ChexSystems

- Banks & Credit Unions That Are ChexSystems Inquiry Sensitive

- What Banks & Credit Unions Do/Don’t Pull ChexSystems?

- How To Use Our Direct Deposit Page For Bank Bonuses Page

- Common Bank Bonus Misconceptions + Why You Should Give Them A Go

- How Many Bank Accounts Can I Safely Open Within A Year For Bank Bonus Purposes?

- Affiliate Links & Bank Bonuses – We Won’t Be Using Them

- Complete List Of Ways To Close Bank Accounts At Each Bank

- Banks That Allow/Don’t Allow Out Of State Checking Applications

- Bank Bonus Posting Times