Deal has expired, view more checking bonuses by clicking here

Update 1/12/2020: Bonus has been extended until 12/31/20. Hat tip to IS250

Update 7/2/19: Deal has been extended until December 31st, 2019. Hat tip to BDB on reddit

Update 3/31/19: Deal has been extended until June 30th, 2019.

Update 2/6/19: Deal is back and valid until March 31st, 2019.

Update 10/17/18: Reposting as the $500 bonus has been pulled early. I’d get this $1,000 bonus done sooner rather than later if you’re interested in it.

Offer at a glance

- Maximum bonus amount: $1,000

- Availability: Account must be opened in branch. [Branch locator]

- Direct deposit required: None

- Additional requirements: See below

- Hard/soft pull: Soft

- ChexSystems: Mixed reports

- Credit card funding: None available in branch

- Monthly fees: $40, avoidable

- Early account termination fee: None

- Household limit: None listed

- Expiration date:

December 31st, 2018 March 31st, 2019 June 30th, 2019

Contents

The Offer

No direct link to offer, in branch only

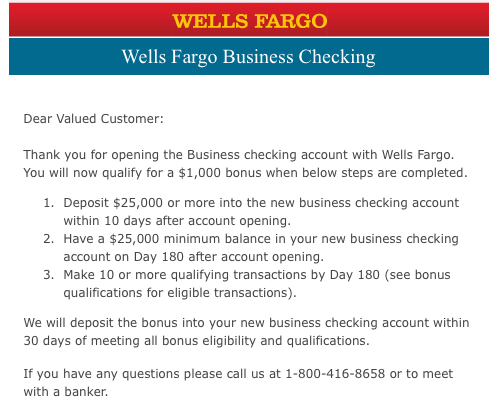

- Wells Fargo is offering a bonus of $1,000 when you open a new platinum business or analyzed business checking account and complete the following requirements:

- Deposit $25,000 or more into the new business checking account within 10 days (might be 30 days, double check your offer) after account opening

- Have a $25,000 minimum balance in your new business checking account on day 180 after account opening

- Make 10 or more qualifying transactions by Day 180 (see below)

The Fine Print

- Eligibility: Unique bonus offer code can only be used once.

- You cannot be:

- A current owner of a Wells Fargo business checking account.

- A Wells Fargo team member.

- The recipient of a business checking bonus in the past 12 months.

- Bonus Qualifications:

- Open a new Wells Fargo Platinum Business Checking or Analyzed Checking Account in a branch by December 31, 2018.

- Fund the new business checking account with a minimum opening deposit of $25.

- Within 10 days of opening your account, deposit $25,000 or more into the new business checking account, and

- Have a $25,000 minimum balance in your account on Day 180, and

- Make 10 or more qualifying transactions that have posted to the new business checking account by Day 180:

- Debit card purchases/payments*

- ACH – Automated Clearing House (credits and debits)

- Checks paid from your new account (deposited and cashed)

- Mobile deposits**

- Wires (credits and debits)

- Wells Fargo Business Bill Pay or Direct Pay

- Bonus Payment:

- We will deposit the bonus into your new business checking account within 30 days after meeting all offer eligibility and requirements.

- Business checking account must remain open to receive the bonus amount.

- You are responsible for any federal, state, or local taxes due on your bonus, and we will report the bonus amount as income to the applicable tax authorities as required by law. Consult your tax advisor.

- All bank account bonuses are treated as income/interest and as such you have to pay taxes on them

Avoiding Fees

Monthly Fees

Business choice is an eligible account and the easiest to keep fee free. This account has a $14 monthly fee that is waived if any of the following requirements are met:

- $7,500 average balance, OR

- $10,000 in combined balances (business checking, savings, time accounts, and credit), OR

- 10 or more posted business debit card purchases/payments1, OR

- A linked Direct Pay2 service, OR

- Qualifying transactions from a linked Wells Fargo Merchant Services account3, OR

- Qualifying transactions from a linked Wells Fargo Business Payroll Services account4

Early Account Termination Fee

There is no early account termination fee.

Our Verdict

Best previous offer has been $500 and that is still available. That bonus is easier to meet the requirements for and easier to keep the account fee free. That being said, this is an extra $500. For this bonus you are realistically going to need the $25,000 deposited for 210 days (180 for the requirements and further 30 for the bonus to post). Still a great return if you have a spare $25,000. We will be adding this to our list of the best checking bonuses.

Big thanks to reader, NIL who let us know. Learn how to find bonuses and contribute to the site here.

Useful posts regarding bank bonuses:

- A Beginners Guide To Bank Account Bonuses

- Bank Account Quick Reference Table (Spreadsheet) (very useful for sorting bonuses by different parameters)

- PSA: Don’t Call The Bank

- Introduction To ChexSystems

- Banks & Credit Unions That Are ChexSystems Inquiry Sensitive

- What Banks & Credit Unions Do/Don’t Pull ChexSystems?

- How To Use Our Direct Deposit Page For Bank Bonuses Page

- Common Bank Bonus Misconceptions + Why You Should Give Them A Go

- How Many Bank Accounts Can I Safely Open Within A Year For Bank Bonus Purposes?

- Affiliate Links & Bank Bonuses – We Won’t Be Using Them

- Complete List Of Ways To Close Bank Accounts At Each Bank

- Banks That Allow/Don’t Allow Out Of State Checking Applications

- Bank Bonus Posting Times